TEXAS, USA — We continue to make our way down the "death checklist", also known as the "life checklist"… because that is cheerier and this stuff needs to be completed while we are still living.

We are finally getting to wills... next time. That’s because wills always get put off. Actually, it’s because even if we have a will -- and certainly if we don’t -- we also need to give special thought to naming beneficiaries on our financial accounts.

We talked about this last summer. Hopefully, you got it done then. But if you didn’t, and even if you did, there’s more to discuss.

Life insurance, IRAs, 401Ks, CDs, checking accounts, savings accounts, brokerage accounts -- all of them have forms for you to select beneficiaries.

A beneficiary is someone you designate to receive all or part of an account to when you die.

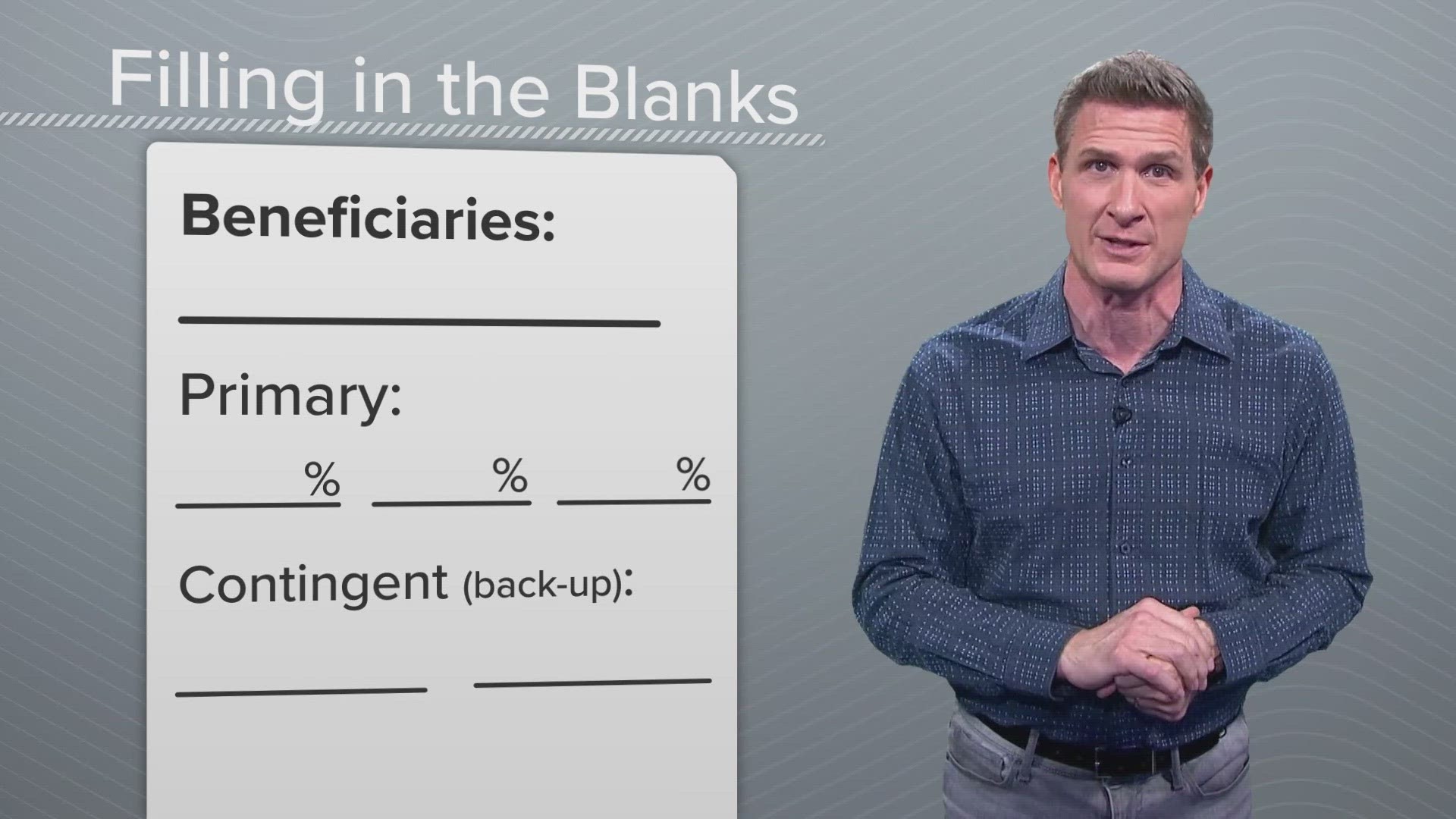

Usually, you can choose one or multiple primary beneficiaries and the percentage each one would get. In case your primary beneficiaries are also deceased when you die, some of these accounts also allow you to choose contingent (back-up) beneficiaries and the percentages they would get.

Beneficiaries or payable on death/transferable on death designees

Depending on the account type, a beneficiary can also be called a payable on death or transferable on death designee. It is a good idea to click the two links in the previous sentence, because even though some people use the labels interchangeably, they have different attributes.

The process of naming beneficiaries can also differ from one institution to another. Some banks require you to make beneficiary selections in person. Others allow you to do it online.

Only about one-third of people surveyed realized that the person named as the beneficiary or the payable or transferable on death designee directly gets the money when they die. But they do. Generally, they would just present their ID and your death certificate, and the account would become theirs right away.

Use with caution: These designations are powerful

It doesn’t take months or even years because it bypasses the lengthy process of probate, which is when a court oversees the distribution of your assets.

So, caution: This is powerful. Even if you have a will, and it says you want to leave "such and such account" to "so and so," but you name "what’s his face" as the beneficiary on that actual account -- the beneficiary designation usually prevails over the will, so "what’s his face" would likely get it.

Make sure the names are spelled exactly right. And make sure this is who you really want to leave the money to.

Maybe you listed your husband as beneficiary, and then he became your ex-husband. You probably don’t want your ex to get your assets. But if you don’t update your selection, that could happen.

So, update these regularly. Maybe make that a day-before-your- birthday chore every year so you remember it.

More words of caution…

As you set about filling in these important blanks on your financial accounts, another caution: As Kiplinger points out in number two of its list of five critical beneficiary mistakes to avoid, there are instances in which naming certain beneficiaries might not be beneficial.

The publication notes that if you name your minor child as a beneficiary, in many cases that child can’t receive the money directly and it could get tied up in a legal process.

If you have a special needs loved ones you list as a beneficiary, that influx of money they receive after you die could suddenly make them ineligible for valuable government benefits.

Also, look out for other potential mistakes when naming beneficiaries.

If you still have questions or concerns about naming beneficiaries and the possible complications of having or not having a will in addition to naming beneficiaries, it may be wise to consult a financial planner and/or an attorney.